People who have lost part of their nest eggs in the recession encounter a hard retirement, but those people who are born between 1981 & 1996, who are called the millennial generation, face the uncertain financial future in America due to the Great Depression. 3 decades of stagnant wages were followed by the best Recession, and the income and the net worth gulf between the rich and the middle class is at its high level in the past 90 years. Below, we will review how financial realism is colliding with this generation’s money habits, which can pose a severe economic dilemma for various people. The media caricature of millennials glosses over how changing customer preferences are driven by complicated factors such as the financial situation of millennials, the ethics they need their products to embody, and their great concentrate on health.

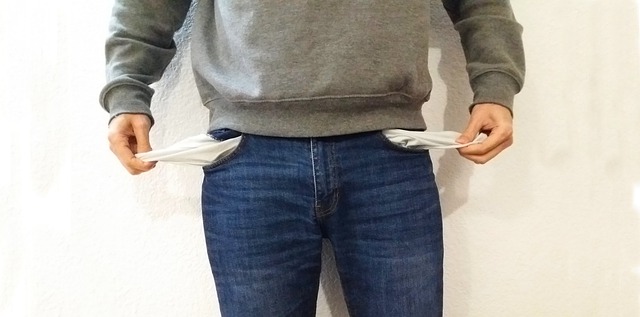

Millennials are in debt.

They earn less, hold some assets, and have less wealth than members of previous generations did when they were their age, as per the Fed. Several are burdened by student loan debt; as median incomes have failed to keep pace with the skyrocketing prices of four-year college programs.

Although American paychecks have increased over the past few decades, the buying power of those paychecks has remained stagnant, as per a recent Pew study.

Managing money that does not go as far when it isn’t tied up in debt payments largely affects how millennials budget and spend.

Millennials value spending their money ethically.

Instead of valuing low costs above all else, 73 percent of millennials are willing to pay more for products and services that are sustainable or help promote a positive effect on the globe. When it comes to investing, millennials are twice to create sustainable investments compared to the average investor, with 75 percent reporting that they think their investment options can influence climate change.

Millennials prioritize health and wellness

millennials generation is very health-conscious than others. 9 in 10 people in this generation believe that it is essential to eat healthily. Millennials are the generation concerned with natural as well as ethical food products, and they account for more than half of organic food consumption.

Millennial Spending Habits

A survey from the American Institute of Certified Public Accountants (AICPA) shows that over 3-quarters of millennials want to have similar clothes, cars, and technological gadgets as their friends and that about half of them have to utilize a credit card to pay for basic everyday necessities like utilities and food. Over 25 percent of them had late payments or are dealing with bill collectors, and well over half are receiving few forms of financial aid from their parents.

One of the disturbing fact of this study shows that 7 out of 10 millennials define financial stability to be capable of paying all the bills every month. The study makes a difference in money habits between the genders, where men feel inclined to keep up with their friends in material goods while women tend to be more frugal and place a high emphasis on saving money.

The Impact of Social Media

Obviously, the pressure that millennials have for conforming to the financial habits of their peers come from social media, where financial milestones such as home and car buying are posted for all to see. Due to the influence of social media, plastic surgery is another place where few millennials are spending their money. Injectables are becoming more famous and social media influencers often post before and after videos online. As per a 2018 survey by the American Academy of Facial Plastic & Reconstructive Surgery, 72 percent of plastic surgeons reported seeing a rise in patients under the age of 30 wanting injectables and cosmetic surgery.

Millennials having a hard time with financial

Millennials can strive for financial independence, but as a whole, they are slow to break out on their own. As per Fidelity Investments’ Study, almost half (47%) of millennials have their parents to pay for certain items for them, like cell phone plans, utilities, TV streaming services. That isn’t to mention the rising number of millennials who are living with their parents, now at 21%. The advantage of this? Millennials are learning to be more prudent with their finances, as 85% say they’ve few forms of savings, up from 77% in 2014, and 59% have set aside an average of $9,100 in an emergency fund. 60% report saving for retirement, up from 51% in 2014. But while millennials are saving, they are hesitant about investing. Of those with an emergency fund, 86% are storing it in a traditional savings account, where it is probably earning less than 0.25% in interest. Additionally, 9% of millennials view themselves as investors, compared to 44% who identify as spenders or 46% who consider themselves savers.

Average Weight Investors Take Risks

Customers come in all sizes and shapes, and as an advisor, you likely do not think much about their appearances. But a new study says this may offer insight into how they invest. A recent study by the University of Miami School of Business Administration discovered that people who are tall and normal weight are willing to take risks and more probably to hold stocks than shorter, overweight, and obese individuals. Especially, an obese person is 10% less probably for investing in stocks than a person of normal weight, while individuals in the top 20th percentile for height are 7.5% more probably for investing in stocks than the low 20th percentile. Why the difference? Confidence and optimism. Overweight individuals tend to be less optimistic, and this can make them more risk-averse. We found that the environmental review one receives because of physical attributes shapes people as well as affects their portfolio decisions.

Calling all Millenials! Our team at YMA Wealth Management Group can assist you in gaining control of your spending to make wiser decisions. Debt? In need of credit repair? We’re here to help you get back on track.

Calling all Millenials! Our team at YMA Wealth Management Group can assist you in gaining control of your spending to make wiser decisions. Debt? In need of credit repair? We’re here to help you get back on track.

Ready to take control of your wealth for a brighter future?

Contact us now: 1-800-381-9206